Buyers Of EquityBuild Properties Score Big

Those who closely monitor the Chicago south side multifamily residential real estate market will know that a company known as EquityBuild was running a massive Ponzi scheme that met its demise on August 17, 2018, when the Securities and Exchange Commission obtained a federal court order halting its operations and placing its assets in receivership. The lion’s share of the fraud was perpetrated upon unsophisticated investors who were lured, typically through Internet advertising or cold calling, to participate in the making of group loans to EquityBuild, which promised to use the funds to purchase and rehabilitate distressed property with the stated intention of reselling 18-24 months later and using the proceeds from the sale to repay the investors (who, in this case, were technically lenders). EquityBuild promised to make monthly interest payments at attractive rates ranging from 15-18% percent per annum with the entire principal balance retired upon the resale.

Generally speaking, and using hypothetical figures, it worked like this: EquityBuild would purchase a property for $800,000 but likely assert that it purchased the property for $1,000,000. Then it would inform the prospective “mom and pop” (and typically out-of-state) lenders that the building required $200,000 in improvements, which when completed would enable EquityBuild to achieve a sufficiently high occupancy at sufficiently high rental rates to justify reselling the building as a stabilized asset to a third-party buyer at a price of at least $2,000,000. The prospective lenders were informed that the “all in” costs would be approximately $1,600,000 – consisting of the (alleged) $1,000,000 acquisition cost, ancillary closing costs, the $200,000 in improvement costs, construction period carrying costs (e.g., property taxes and insurance), and financing costs (i.e., the monthly interest owed to the investor-lenders). Yes, EquityBuild raised the entire interest reserve from the lenders, who were not astute or experienced enough to hold those funds back from the amount that would otherwise be disbursed to cover the project costs. As a result, EquityBuild retained no equity in the property: It purchased the asset for $800,000 and received $1,600,000 from the participating lenders – every nickel up-front.

What could possibly go wrong?

A lot.

EquityBuild rarely made the promised improvements. It diverted the loan proceeds to other Ponzi scheme expenses, including the payment of outstanding amounts of undisclosed fees to the principals and the payment of interest to other groups of lenders who participated in loans secured by unrelated properties. The buildings became magnets for City inspectors who cited the company for hundreds of code violations, which consistently bled cash. By the time 18-24 months had come and gone, the property was worth little (if any) more than what EquityBuild originally paid for it (and EquityBuild frequently overpaid because it needed a steady pipeline of inventory to feed the pyramid scheme). The company could not resell the property for a price that would retire the lender debt, so EquityBuild would make false assurances about impending dispositions and extend the loans to buy additional time. When all else failed, it ultimately turned to a new set of private lenders for millions of dollars in refinancing proceeds, and, to effectuate those refinancings, it secretly released the mortgages that secured the existing debt. It was a house of cards destined to collapse -- as it finally did.

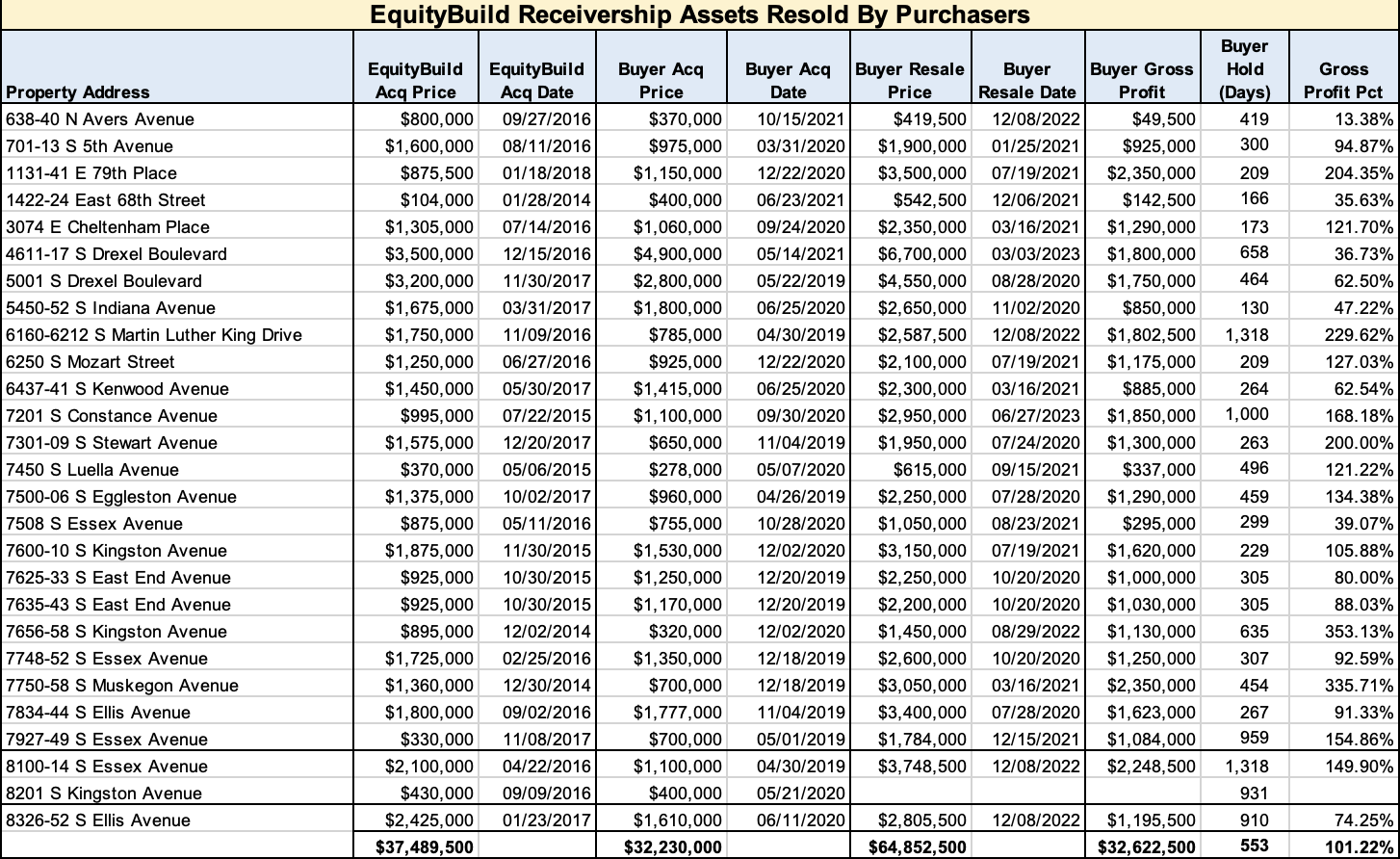

Following the implosion, the receivership estate was forced to sell nearly 120 properties, and to accomplish that feat it turned to Jeffrey Baasch and Finley Askin, two experienced investment sales advisors. The properties were marketed in tranches, and the sales were conducted through a highly publicized, blind auction that produced the highest possible offers. Though every effort was made to avoid the appearance of distressed sales (or a liquidation event), the bidders were fully aware that the receiver was under pressure to sell a substantial amount of property. So it became a dream scenario for opportunistic buyers.

Charts reflecting the results to-date appear below. As of this writing, the first 30 multifamily properties purchased from the receivership and resold to new buyers consistently generated lucrative returns. The actual net profits cannot be ascertained because the public records do not disclose expenditures on capital improvements or data reflecting net operating income (or loss), but the gross profits speak for themselves. In absolute terms they demonstrate consistent success.